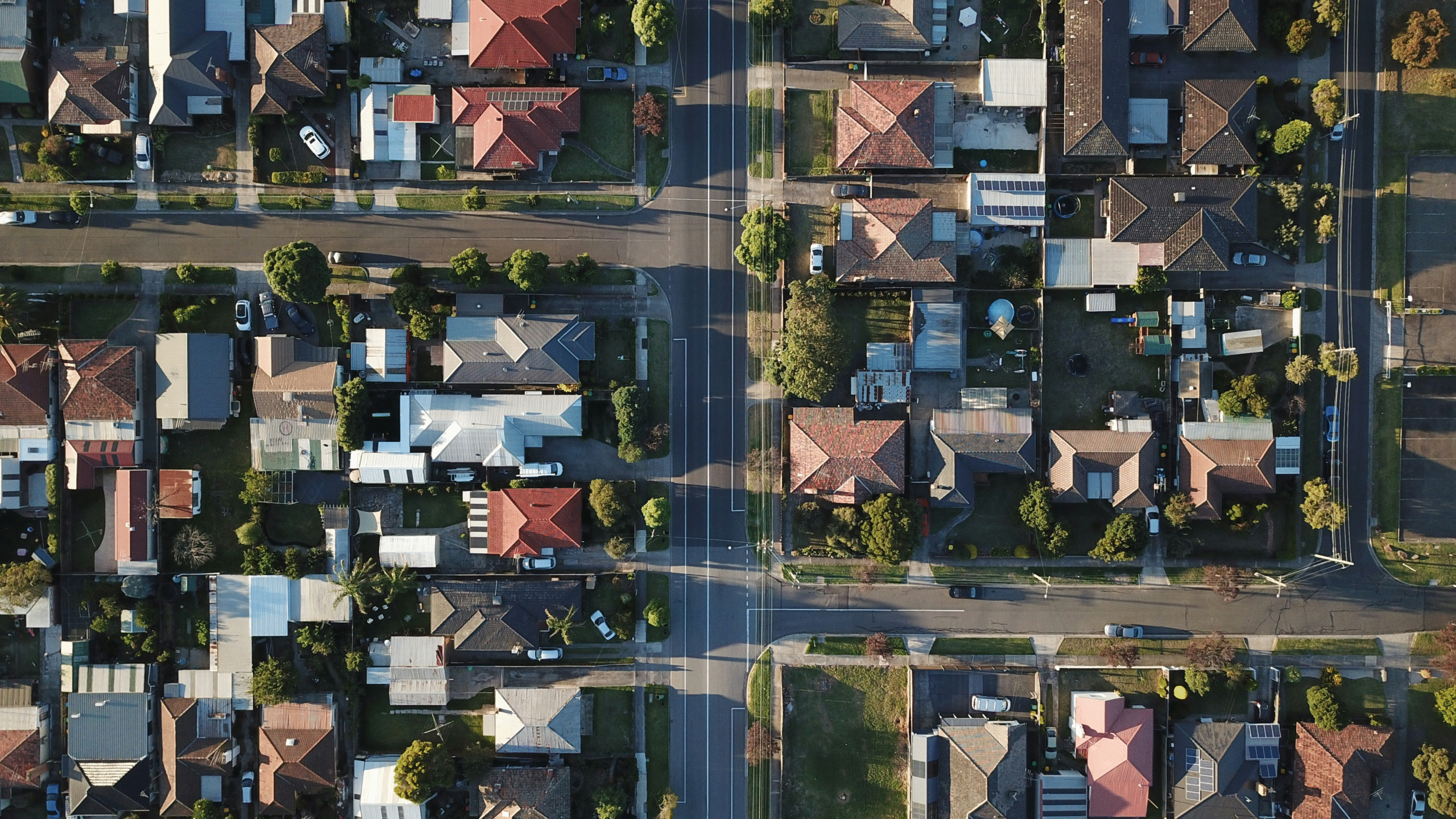

For decades, Australia’s housing market has shown a resilience that puzzles observers abroad. Property values may dip briefly, but they rarely fall for long before beginning their climb again. Even in moments of global disruption – from the Asian Financial Crisis to the Global Financial Crisis, from the pandemic to the sharpest interest rate rises in a generation – Australian housing has bent but not broken. For many, it feels as though prices can only ever go in one direction.

The explanation lies not in luck, but in structure. Successive governments have built and maintained a system of tax incentives, lending practices, and policy settings that have made property not only a source of shelter, but also the dominant vehicle of wealth. Combined with strong migration and cultural preference for homeownership, these factors have created a market that is highly resistant to sustained downturns.

How tax and policy drove rising property prices

Central to this structure is negative gearing. The provision, which allows investors to deduct rental losses from their taxable income, has been in place in some form since the 1930s. It became politically salient in the 1980s when the Hawke–Keating Labor government attempted to restrict it, only to reinstate it two years later after concerns about rising rents. Negative gearing makes it possible for investors to carry properties that cost more to run than they return in rent, because the shortfall reduces their annual tax bill.

The other cornerstone is the capital gains tax discount. Capital gains tax was introduced in 1985 to ensure profits from the sale of assets were taxed fairly. Fourteen years later, the Howard government changed the rules, halving the taxable gain on assets held longer than 12 months. The intention was to simplify the system and encourage long-term investment. In practice, it meant that property investors could claim losses against their salary today and pay tax on only half their profits in the future. The combination created one of the most generous investment frameworks in the developed world.

What matters as much as the policies themselves is their stability. Negative gearing and the CGT discount have been preserved by both sides of politics for decades. Labor governments introduced them; Coalition governments expanded them. Even after the bruising 2019 election, when Labor campaigned on limiting negative gearing to new builds and halving the CGT discount, the backlash was so strong that the party has since ruled out further attempts. That bipartisan continuity has given investors confidence that the rules will not change suddenly, reinforcing property’s appeal as a long-term wealth strategy

The Australian property market is a global outlier

Australia’s approach looks unusual when compared with peers. In France and Germany, renting is widespread and socially accepted, supported by strong tenant protections and long-term leases. Mortgages are conservative, speculative investment is discouraged, and homeownership is less of a cultural imperative. The United States offers lower tax rates on long-term capital gains, but losses on rental properties are capped, and mortgages are often fixed for 30 years, insulating households from rate rises. The United Kingdom phased out full mortgage interest relief in 2020, replacing it with a limited credit, while Canada taxes half of all capital gains but places tighter limits on loss deductions. New Zealand went further, removing most interest deductibility for investment properties in 2021.

Few countries combine broad negative gearing with a 50 per cent capital gains discount. In that sense, Australia has built an especially supportive environment for property investment, which helps to explain why downturns have historically been short-lived.

Negative gearing on property mostly enjoyed by the rich

Around 2.2 million Australians hold an interest in rental property. Most of them are small investors: close to three-quarters own a single dwelling, while less than one per cent own six or more. The image of the country dominated by landlords with sprawling portfolios is the exception rather than the rule.

Yet the financial benefits of the system are concentrated at the top. According to Treasury and Parliamentary Budget Office analysis, the top 20 per cent of income earners claim about 60 per cent of all negative gearing deductions. The top 10 per cent capture around 80 per cent of the value of the capital gains tax discount. This means that while many Australians participate, the largest financial advantages accrue to a relatively small, high-income group.

This concentration reflects how the system rewards those with the capacity to borrow and hold multiple properties. Professionals with stable, high salaries – doctors, lawyers, executives – can use property to diversify their wealth portfolios, sustain short-term losses, and realise long-term gains

High debt levels make monetary policy changes risky

Another defining feature of the system is the level of household leverage. Australian households carry debt worth around 190 per cent of disposable income, placing them among the most indebted in the world. Only Denmark and the Netherlands carry similar ratios, while Canada and Norway are close behind. The contrast with the United States, where the figure sits at around 100 per cent, or with Germany and France, closer to 90 to 100 per cent, is stark.

The structure of Australian mortgages magnifies this effect. Unlike in the United States, where households often lock into 30-year fixed-rate loans, Australian borrowers are usually on variable or short-term fixed contracts. That means interest rate changes flow quickly into household budgets.

For the Reserve Bank of Australia, this creates a policy dilemma. Raising interest rates curbs inflation but hits mortgage holders hard, forcing them to cut back on spending. Leaving rates low avoids household stress but risks allowing price pressures to linger. Monetary policy becomes a sharper but narrower instrument, powerful in the short term but constrained overall.

Why the property market rarely crashes

Despite high leverage, the housing market has proved remarkably resistant to prolonged corrections. There are several reasons. Investors with high incomes are able to absorb short-term losses and hold through downturns. The tax system rewards them for doing so, with negative gearing softening the pain today and the CGT discount offering a lighter tax burden tomorrow.

Governments have historically stepped in with grants or construction stimulus when the market wobbles, providing a backstop.

Banks, which have more than half their lending tied to mortgages, have an incentive to maintain stability, and regulators are acutely aware of the financial system’s exposure. Migration also plays a central role. Population growth adds steady demand for housing, both in the rental market and eventually in ownership, ensuring that the underlying need for dwellings rarely abates.

Taken together, these dynamics mean that housing downturns tend to be shallow and short-lived. When the market does soften, buyers often step in quickly, confident that long-term fundamentals will support values.

Australia’s addiction to property has trade-offs

Australia’s reliance on property as a wealth engine has broader implications. The flow of capital into housing means less is available for other forms of investment. Entrepreneurs often struggle to raise finance compared with property investors, because banks see housing as safer collateral. Critics argue this dampens innovation and productivity growth, though defenders note that stability has its own economic benefits.

The distribution of wealth is also affected. Rising property values have benefited those who already own homes, particularly older generations, while younger Australians face higher barriers to entry. Access to family wealth increasingly determines who can step onto the property ladder. At the fiscal level, the cost of negative gearing and CGT concessions runs into the billions each year, revenue that could otherwise fund services or infrastructure. But political consensus has long held that the benefits to household wealth and market stability outweigh these costs.

Plans to change the CGT discount

While governments have largely avoided touching these policies, debate has not disappeared. In August 2025, the Australian Council of Trade Unions proposed limiting negative gearing and the CGT discount to a single investment property per taxpayer. Investors would have a five-year transition period to adjust, after which concessions on additional properties would no longer apply.

Analysis of Australian Taxation Office data suggests the change would affect about 306,000 investors, or roughly one in seven. Most would be unaffected: of the 1.1 million negatively geared investors, more than 800,000 hold just one property. The ACTU estimates the reform could raise around $1.5 billion annually, which could be directed towards social and affordable housing.

The Parliamentary Budget Office has also modelled scenarios that phase out concessions for multiple properties, estimating revenue gains of nearly $6 billion over the forward estimates period. The Greens have already indicated support for the ACTU plan, meaning the Albanese government would have the numbers to pass it if it chose to act.

Yet political caution prevails. After the 2019 election loss, Labor has been reluctant to revisit the issue. Senior ministers insist the government has “no plans” to change negative gearing or the CGT discount. The calculation is clear: while reforms might appeal to younger voters struggling with affordability, they risk alienating the millions of Australians whose wealth is tied up in investment property.

Lessons from abroad

Other countries offer a glimpse of how alternative paths might look. France and Germany have avoided speculative surges through heavier taxation of property wealth and stronger rental protections. The United States, chastened by the subprime crisis, has benefited from a mortgage system that spreads risk differently. Canada and New Zealand, facing affordability pressures similar to Australia’s, have begun rolling back concessions in recent years.

Australia has chosen a different model, one that embeds property at the heart of household and national wealth. That model has produced stability and resilience, but it also creates dependence.

Conclusion

Australia’s housing market feels built to last because, in many ways, it has been built that way. Tax incentives, political continuity, cultural preference, and financial structure all combine to reinforce the role of property as the country’s central wealth vehicle. The result is a system where downturns are cushioned, policy is calibrated with housing in mind, and migration continually refreshes demand.

The trade-offs are well known: high household debt, skewed wealth distribution, and heavy fiscal costs. Yet for investors, the key fact remains that Australian property operates within a framework designed to sustain long-term confidence.

No market is immune to cycles, but the Australian housing system explains why, for decades, property has felt like one of the most enduring investment stories in the developed world.