Breaking News

Popular News

Enter your email address below and subscribe to our newsletter

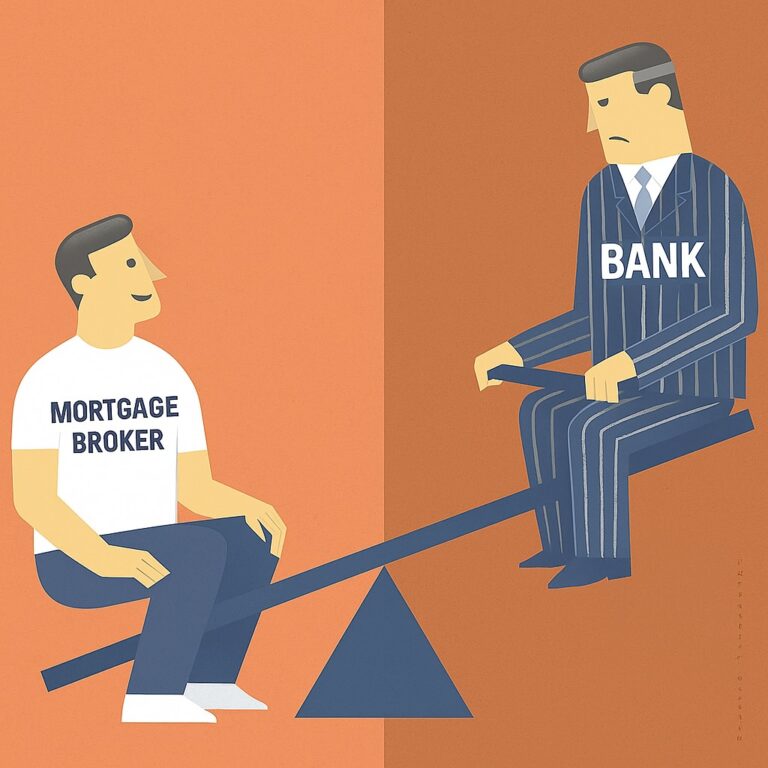

In Australia’s home-loan market, the role of the mortgage broker often seems straightforward: you meet them, they help you find a loan, you settle on a property, and all is done. But beneath that simplicity lies a vital financial anatomy that matters not only for understanding costs, but for judging alignments and incentives. Here’s how it works -and what you probably didn’t kn

When you engage a broker in Australia, you’ll often do so under the assumption that the service is “free” to you. That’s broadly correct: in most residential lending cases, you won’t pay the broker directly. Rather, the lender pays the broker a commission after the loan settles.

There are two principal types of payments:

At first glance, “free to you” sounds like a win – and broadly it is. But as with most things behind the finance scenes, the full story carries nuance.

Here is a detail many borrowers overlook: claw-back clauses and how offset account balances can reduce the commission a broker receives.

When a loan is discharged or refinanced within a certain period (often 1 – 2 years), the lender may require the broker to repay part or all of the upfront commission. That means if you switch your loan too quickly, the broker loses earnings. In that sense, if you intend to refinance early – for renovations, for example – it’s often best to mention this upfront to the broker so they know your intentions. Also, to ensure that you don’t get hit with discharge fees, application fees, and other potential break costs in the refinancing process.

Something else to consider: some lenders calculate the upfront or trailing commission on the net draw-down (loan amount minus any offset account balances). If you settle a $500,000 loan but have $100,000 in the offset, the broker’s commission might be calculated on $400,000.

Australia’s regulatory regime tries to ensure brokers act for your interest, regardless of how they’re paid. For instance, under the “best-interests” duty, brokers must prioritise your needs when recommending a home loan.

However – a subtle but important point – lenders themselves are not bound by that same best-interests duty when dealing directly with you. That means using a broker can provide an additional assurance of impartial advice

To safeguard your interests and understand how their incentives work, consider raising the following:

The payment structure of brokers in Australia has subtleties that matter. Understanding upfront vs trail commissions, claw-back conditions and offset-balance effects gives you better leverage as a borrower and helps align expectations. In a sense, it puts you on a firmer footing to ask: “Is this loan the best for me – or the one that pays best for my broker?”

And that question matters, because in the home-loan journey, the difference between “good” and “great” often resides in the details.