Compare investment property loans in Australia

Find competitive loan rates for buying an investment property or rental property.

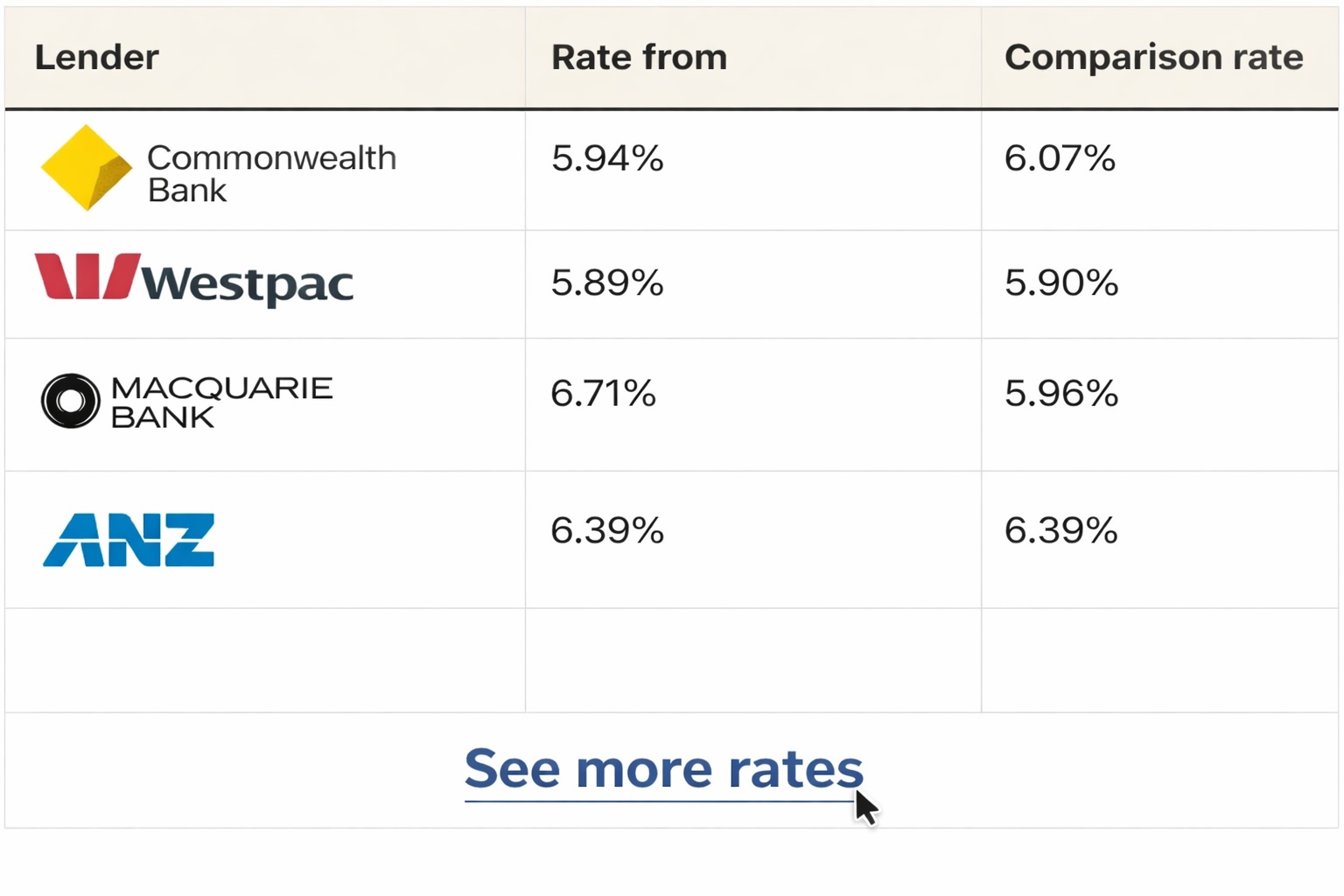

Compare investment loans from top lenders

| Lender | Rate from | Comparison rate | Loan type | Check your eligibility |

| 5.69% | 5.82% | Variable | ||

| 5.64% | 5.65% | Variable | ||

| 6.46% | 6.50% | Variable | ||

| 6.14% | 6.14% | Variable | ||

| 5.69% | 5.71% | Variable | |

| 5.79% | 5.82% | Variable | ||

| 5.63% | 5.65% | Variable | ||

| 5.95% | 5.95% | Fixed | ||

| 5.74% | 5.75% | Variable |

What is an Investment Property Loan?

An investment property loan is a home loan used to purchase a property that will generate income, usually through renting the property to tenants. In Australia, these loans are commonly used to buy houses, apartments, or units that are rented out long-term or used for short-stay accommodation.

Investment property loans usually have slightly higher interest rates than owner-occupier home loans because lenders consider them higher risk. Banks assess both your personal income and the expected rental income from the property when deciding how much you can borrow.

Most lenders require a deposit of around 20% of the property value to avoid lenders mortgage insurance (LMI), although some investors may borrow with a smaller deposit depending on their financial situation.

Investment loans may also offer interest-only repayment options, which many property investors use to reduce repayments during the early years of owning a rental property.

How to Qualify for an Investment Property Loan

To qualify for an investment property loan in Australia, lenders assess several factors to determine whether you can comfortably repay the mortgage.

Deposit requirements: Most lenders require a deposit of at least 20% of the property price for an investment loan. Borrowing more than 80% of the property value may require lenders mortgage insurance (LMI).

Income and employment: Banks assess your salary, employment stability, and other income sources to determine whether you can afford the loan repayments. Self-employed borrowers may need to provide additional financial records.

Rental income assessment: When buying an investment property, lenders usually include expected rental income when calculating your borrowing capacity. However, banks often only count 70–80% of the expected rent to allow for vacancy periods and expenses.

Credit score: A strong credit history and credit score improves your chances of being approved for an investment property loan and may help you secure a more competitive interest rate.

Borrowing capacity: Your borrowing capacity depends on your income, expenses, existing debts, and the expected rental income from the investment property.

Quick guide to investment property loans

Investment property loans are home loans used to purchase rental or income-producing property.

✓ Interest rates are often slightly higher than owner-occupier home loans because lenders consider investment loans higher risk.

✓ Most lenders require a deposit of around 20% to avoid lenders mortgage insurance (LMI).

✓ Banks usually assess both personal income and expected rental income when calculating borrowing capacity.

✓ Lenders often count 70–80% of expected rental income when assessing your application.

✓ Borrowers with strong credit scores and stable income may qualify for more competitive loan rates.

✓ Many investors use equity in their existing home to fund the deposit for an investment property.

✓ Lenders typically allow borrowing up to 80% of the property value (80% LVR) without lenders mortgage insurance.

✓ Investment loans may offer variable, fixed, or interest-only repayment options.

✓ Comparing lenders can help investors find lower interest rates and better loan features.

Using Equity to Buy an Investment Property

Many property investors use equity in their existing home to fund the deposit for an investment property.

Home equity is the difference between the current value of your property and the remaining balance on your mortgage. If your home has increased in value, you may be able to refinance or take out a new loan to access that equity.

This strategy allows investors to purchase property without needing large cash savings, using the value built up in their home instead.

Most lenders allow homeowners to borrow up to 80% of the property’s value, known as the loan-to-value ratio (LVR).

Example of using equity:

Home value: $900,000

Current mortgage: $500,000

Maximum borrowing at 80% LVR: $720,000

Available equity: about $220,000

This equity could potentially be used as a deposit for an investment property.

Current Investment Property Loan Rates in Australia

Investment property loan rates vary depending on the lender, loan features, and whether the loan has a fixed or variable interest rate.

Variable investment loan rates: Variable rate loans move up and down with changes in the lender’s interest rates. They often offer more flexibility, including offset accounts and extra repayments.

Fixed investment loan rates: Fixed rate investment loans lock in the interest rate for a set period, usually between one and five years, which can provide certainty about repayment amounts.

Interest-only investment loans: Many investors choose interest-only home loans, where repayments initially cover only the interest on the loan rather than the loan principal. This can reduce repayments during the early years of property ownership, although repayments typically increase once the interest-only period ends.

Investment loan rates differ between lenders based on factors such as loan size, deposit amount, borrower income, and property type, which is why comparing lenders can be important.

How Investors Finance Multiple Properties

Experienced property investors often use a range of strategies to build a portfolio of investment properties over time.

Equity recycling: As property values increase, investors may access additional equity in their existing properties to fund deposits for future property purchases.

Refinancing investment loans: Refinancing allows investors to switch lenders or loan products to secure lower interest rates, better loan features, or to release equity for additional investments.

Cross-collateralisation: Some investors structure loans using multiple properties as security for one loan, known as cross-collateralisation. This can increase borrowing power but may also reduce flexibility when selling properties.

Property portfolio growth: By combining rental income, property price growth, and strategic refinancing, many investors gradually expand their property portfolio over time, purchasing additional investment properties as their borrowing capacity increases.

Investment Property Loan FAQs

Yes. An investment property loan is designed for properties that will generate rental income rather than being lived in by the borrower. Because lenders view investment properties as higher risk, interest rates are often slightly higher than owner-occupier home loans. Banks also assess expected rental income and may apply stricter lending criteria when calculating borrowing capacity.

Investment property loans usually have higher interest rates because lenders consider them riskier than owner-occupied home loans. If borrowers experience financial difficulty, lenders believe they are more likely to prioritise repayments on their primary residence. To account for this additional risk, banks often charge a slightly higher interest rate on loans used to purchase rental properties.

Most lenders require a 20% deposit to purchase an investment property. Borrowing more than 80% of the property value typically requires lenders mortgage insurance (LMI). Some investors purchase property with deposits as low as 10% or even 5%, but this usually involves higher costs, stricter lending requirements, and LMI premiums.

You may need lenders mortgage insurance (LMI) if your deposit is less than 20% of the property value. LMI protects the lender if the borrower defaults on the loan. For investment properties, LMI premiums can be higher than for owner-occupied loans, so many investors aim to contribute at least a 20% deposit to avoid the extra cost.

Yes. Most lenders include expected rental income when assessing your borrowing capacity. However, banks typically only count 70 – 80% of the expected rent to allow for vacancy periods, maintenance costs, and other property expenses. This helps ensure borrowers can still afford repayments if rental income fluctuates.

Interest rates for investment property loans depend on the lender, deposit size, and loan features. In general, investment loan rates are slightly higher than owner-occupier loan rates, although the difference may only be around 0.1% to 0.5% depending on the lender and loan type.

Yes. Many investors choose interest-only investment loans, where repayments initially cover only the interest portion of the loan rather than both interest and principal. This can reduce monthly repayments during the interest-only period, which typically lasts one to five years. However, repayments usually increase once the loan switches to principal-and-interest repayments.

Yes. Many investors use equity in their existing home as a deposit for an investment property. If your home has increased in value, lenders may allow you to refinance and access part of that equity. Most banks allow borrowing up to 80% of the property value, which can then be used to fund deposits or investment costs.

Common features investors look for include:

• Offset accounts to reduce interest costs

• Interest-only repayment options

• Redraw facilities

• Flexible refinancing options

• Competitive variable or fixed interest rates

Comparing lenders can help investors find loans with the most suitable features for their strategy.

Investment property loans typically come in three main types:

• Variable rate loans, where the interest rate can change over time

• Fixed rate loans, where the interest rate is locked for a set period

• Interest-only loans, where borrowers initially pay only interest

Each loan type offers different levels of flexibility, repayment certainty, and cost.

Investors should pay attention to several factors, including:

• high interest rates

• large annual fees

• limited repayment flexibility

• restrictions on refinancing

• expensive lenders mortgage insurance

Comparing multiple lenders and loan features can help investors avoid costly loan structures.

Yes. The best investment property loan depends on factors such as interest rate, fees, repayment flexibility, and loan features. Some lenders offer better terms for investors, including lower rates or interest-only options. Comparing loans from multiple lenders can help investors find the most suitable financing option.

In some cases, yes. Lenders often apply stricter lending criteria for investment loans because they are considered higher risk. Borrowers may need stronger income, larger deposits, or higher credit scores compared with owner-occupier loans.

Yes. Investors can refinance investment property loans to secure a lower interest rate, access equity, or switch lenders. Refinancing may reduce loan costs or improve loan features, although borrowers should consider refinancing fees and lender requirements.

There is no legal limit on the number of investment properties you can own in Australia. However, lenders will assess borrowing capacity, income, existing debt, and rental income to determine whether you can afford additional property loans.

The loan-to-value ratio (LVR) measures how much you borrow compared with the value of the property. For example, borrowing $400,000 on a $500,000 property results in an 80% LVR. Many lenders prefer investment loans with 80% LVR or lower because this reduces risk.

Generally, an investment property loan is intended for properties that will be rented out rather than lived in by the borrower. If you move into the property later, lenders usually require you to notify them because the loan was originally approved as an investment loan. In some cases, borrowers refinance the loan to an owner-occupier home loan if they decide to live in the property permanently.

Yes. If you decide to move into a property originally purchased as an investment, you may be able to refinance the loan as an owner-occupier mortgage. Owner-occupier loans sometimes have lower interest rates, so borrowers occasionally refinance when their circumstances change.

Sometimes. Lenders may apply stricter serviceability calculations for investment loans, particularly if the borrower already owns property or has multiple mortgages. Banks may also apply higher assessment interest rates when calculating borrowing capacity for investors.

Investment property loans usually have a loan term of around 25 to 30 years, similar to standard home loans. Some investors choose interest-only periods for the first few years, after which the loan converts to principal-and-interest repayments.

Many lenders allow offset accounts on investment property loans, although availability depends on the specific loan product. An offset account can reduce the amount of interest paid by offsetting savings against the loan balance.

The best option depends on the investor’s strategy. Variable rate investment loans offer more flexibility and features such as offset accounts, while fixed rate loans provide repayment certainty for a set period. Some investors split loans between fixed and variable rates to balance stability and flexibility.

Some lenders may apply different lending criteria for short-term rental properties, such as Airbnb properties. Rental income projections may be assessed more conservatively because short-stay income can fluctuate more than long-term lease income.

Interest paid on an investment property loan is generally tax deductible in Australia, because the loan is used to generate rental income. Investors should seek advice from a tax professional to understand how negative gearing and other deductions may apply to their situation.

Yes. Many investors purchase rental properties while still paying off their own home. Lenders assess existing mortgage commitments, income, expenses, and rental income projections to determine whether borrowers can afford the additional loan.

Yes, although higher interest rates can reduce borrowing capacity and increase loan repayments. Many investors compare lenders carefully and structure loans strategically to ensure the rental income and long-term capital growth potential support the investment.

Investment loans may include establishment fees, ongoing loan fees, valuation fees, and refinancing costs depending on the lender and loan type. Comparing lenders can help investors understand the total cost of borrowing beyond the interest rate alone.

Many property investors choose to work with mortgage brokers who specialise in investment lending, because brokers can compare multiple lenders and structure loans to suit long-term investment strategies.